Weekly Commentary for the week ending September 20, 2024

A Dovish Fed Pivot and Economic Resilience Drive Market Gains

The past week has been a momentous one for U.S. equities, with the S&P 500 setting a fresh all-time high before paring gains on Friday. This marks the 39th record close of the year for the index, showcasing the market's resilience amid a rapidly evolving economic landscape. The Russell 2000 also enjoyed a strong run, capping a seven-day streak of advances before a slight dip on Friday. This positive performance across equities has been underpinned by two key developments: the Federal Reserve's long-anticipated dovish pivot and continued economic data supporting a soft-landing scenario.

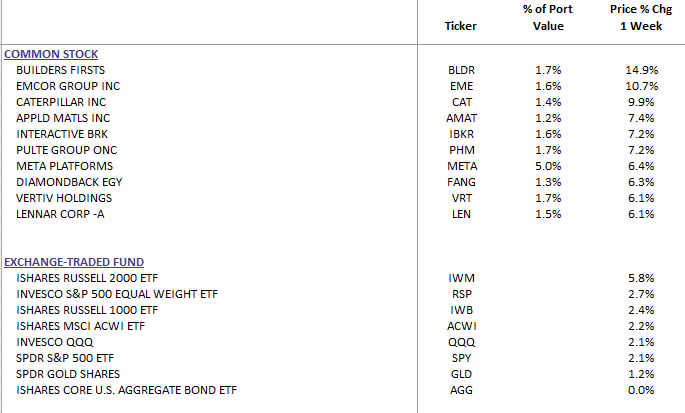

WealthTrust Long Term Growth Portfolio Weekly Top 10

Federal Reserve’s Decisive Action

After months of speculation, the Fed initiated its much-anticipated easing cycle with a 50 basis point (bp) rate cut. This move was widely expected by futures markets but came as a surprise to many analysts who had predicted a more conservative 25bp cut. The Fed’s latest Summary of Economic Projections (SEP) reveals expectations for an additional 50bp in cuts by year-end and a further 100bp in 2025. Fed Chair Jerome Powell emphasized the necessity of this “appropriate recalibration” to avoid falling behind the curve, signaling the central bank's commitment to remaining data-dependent and responsive to potential labor market slowdowns.

The market's response was swift and positive, with equities rallying sharply on Thursday. This reaction reflects a broader sentiment that the Fed’s proactive stance will support continued economic growth, even as some volatility persists. Historically, such easing cycles have been followed by robust equity performance, and many investors are hopeful that this pattern will hold true once again.

Economic Data Supports Soft-Landing Narrative

The Fed’s dovish pivot was complemented by a series of generally upbeat economic reports. Notably, August retail sales defied expectations for a decline, posting a slight increase driven by favorable weather and strong back-to-school shopping trends. Additionally, manufacturing indices from the New York and Philadelphia Federal Reserve unexpectedly turned positive in September, adding to the optimistic outlook.

Other positive data points included the lowest level of initial jobless claims since May and better-than-expected August housing starts and permits. Homebuilder sentiment also improved in September after four consecutive months of decline, further bolstering the case for a soft landing.

Sector Performance and Market Dynamics

The market’s gains were broadly supported across various sectors, with the “Magnificent Seven” tech stocks mostly higher. META (Meta Platforms) led the charge with a 7.0% gain, while NVDA (NVIDIA) saw a slight decline. Other notable outperformers included banks, credit cards, asset managers, life insurers, and industrial sectors such as autos, machinery, and homebuilders. On the other hand, managed care, MedTech, and semiconductors lagged behind, reflecting some sector-specific headwinds.

In the bond market, Treasuries were mostly weaker, with the yield curve steepening as the 2/10 spread ended the week with nearly 15 basis points in positive territory. The U.S. dollar saw mixed performance, weakening against the euro and sterling but strengthening against the yen amid the latest developments from the Bank of Japan. Commodities also had a strong week, with gold rising 1.4% to a new record high and WTI crude oil climbing 3.4%.

Corporate Highlights

Corporate news was relatively light, though there were some notable developments. LUNR surged 49.3% after securing a ~$4.8 billion NASA contract, while CEG rallied 30.1% on the back of a 20-year power purchase agreement with Microsoft. Conversely, PM (Philip Morris) fell 3.8% after announcing the sale of its asthma-inhaler segment Vectura at a fraction of its 2021 purchase price. FDX (FedEx) also struggled, dropping 11.1% after missing earnings expectations and lowering guidance due to reduced demand for priority services.

Looking Ahead

As we move into next week, the market is expected to be light on catalysts, with a sparse earnings calendar and key economic releases including September flash PMIs, consumer confidence, and August new home sales. The Fed will be in focus again with numerous speeches scheduled from governors and regional presidents, providing further insights into the central bank’s outlook. Additionally, the potential for a government shutdown looms as the market monitors developments in government funding legislation ahead of the September 30th deadline.

Conclusion

The past week’s market performance underscores the importance of remaining vigilant and responsive to both economic data and policy developments. The Fed’s dovish pivot, combined with resilient economic indicators, has provided a solid foundation for continued market gains. However, investors should remain mindful of potential risks, including elevated valuations, geopolitical uncertainties, and the upcoming U.S. presidential election. As always, diversification and a long-term perspective will be key to navigating the evolving investment landscape.