Weekly Commentary for the week ending October 4, 2024

As we move into the final quarter of the year, the U.S. equity markets continue to display resilience despite ongoing volatility. This week, both the S&P 500 and Nasdaq extended their winning streaks to four weeks, buoyed by stronger-than-expected economic data. Friday's blowout September jobs report was the catalyst, reversing mid-week declines and bolstering optimism around the much-discussed "soft landing" scenario.

Several sectors shone brightly, particularly China tech, energy, and drug stores, while laggards included athletic apparel, trucking, and EVs. The week ended with mixed performances in big tech, adding a layer of complexity to the market's outlook. Meanwhile, Treasury yields surged after the jobs report, the dollar posted its best week in over a year, and WTI crude saw its largest weekly gain since March, rising 9.1%.

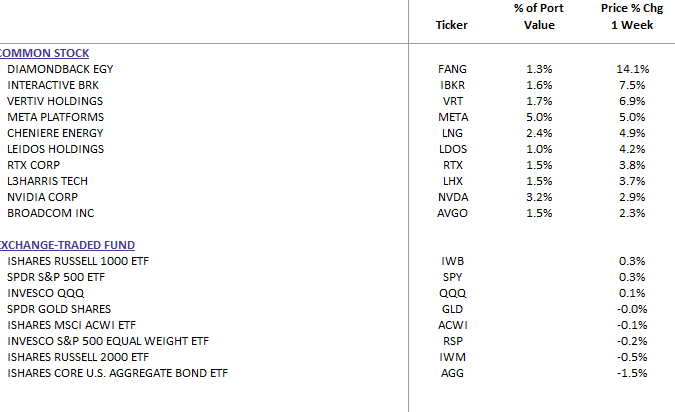

WealthTrust Long Term Growth Portfolio Weekly Top 10

What’s Driving the Market?

A few key factors fueled this week’s activity.

First, the economic data continues to support the narrative of a soft landing. September payrolls significantly outpaced expectations at 254,000, beating the consensus estimate of 150,000. The labor market remains tight, and while recession fears have not disappeared, this report added another layer of confidence to the growth outlook. Notably, the unemployment rate ticked down to 4.1%, while wages remained strong, giving a boost to consumption trends.

In addition to jobs, other data points added to this positive narrative. The JOLTS report showed job openings rebounding, and while ISM Manufacturing came in slightly below consensus, the production index surged, signaling strength in output. ISM Services also posted a better-than-expected reading, though the rise in the prices index highlights the lingering inflation concerns.

The macroeconomic backdrop is increasingly important as we consider Fed policy. Despite hawkish repricing, the market still expects rate cuts by mid-2025. However, Fed Chair Jerome Powell’s comments this week underscored the central bank's cautious approach, noting that the Fed isn’t in a hurry to cut rates. This contrasts with dovish updates from other global central banks, such as Japan and the UK, which are showing greater openness to cutting rates sooner.

A Shift in Global Focus: Geopolitical Tensions & Energy Prices

Geopolitical risk also made headlines this week, with tensions escalating in the Middle East. Israel’s actions in Beirut and a potential Iranian retaliation add a layer of uncertainty. This unrest pushed oil prices higher, which has potential implications for inflation and the global economic outlook.

Energy stocks were the clear winners this week, as WTI crude surged. This marked the sector's best performance since March, further reinforcing its role as a critical hedge in portfolios, especially in periods of geopolitical instability.

Mixed Corporate Updates: A Preview of Earnings Season

Corporate news was light ahead of the upcoming earnings season, but we did see some notable developments. Nike’s decision to pull FY25 guidance due to its CEO transition caught investors' attention, as did weak sales figures from Levi’s and ConAgra, which both missed estimates and cut their revenue guidance. These earnings misses serve as a reminder of the challenges that persist for consumer-facing sectors.

Big tech remains a mixed bag. Nvidia’s CEO spoke positively about demand for its AI chips, while reports suggested that Apple might cut orders for key semiconductor components. Tesla, on the other hand, saw a miss in Q3 deliveries, contributing to a broader underperformance in the auto complex this week.

What to Watch Next Week

Looking ahead, earnings season officially kicks off next week, with major names like PepsiCo, Delta, and the big banks (JPMorgan, Wells Fargo, Bank of New York Mellon) set to report. These earnings reports will provide key insights into the health of corporate America as we approach year-end.

Next week will also see the release of important macro data, including September's CPI and PPI reports, which will shed more light on inflationary pressures. Additionally, Treasury auctions will dominate headlines, as the government plans to sell $58B in 3-year notes, $39B in 10-year notes, and $22B in 30-year bonds.

Sector Performance: A Week of Divergence

From a sector perspective, Energy led the way, gaining over 7% on the back of rising oil prices. Communication Services and Utilities also outperformed, while Materials and Real Estate were among the biggest laggards. Notably, Technology was flat for the week, highlighting the mixed sentiment around big tech as AI optimism continues to clash with broader concerns about growth and valuations.

Navigating Uncertainty with Strategic Allocation

As we move into earnings season, market volatility is likely to persist. The combination of geopolitical tensions, inflationary pressures, and shifting central bank policies means investors must remain vigilant. However, there are still opportunities in select sectors, particularly energy, financials, and communication services.

For long-term investors, this is a time to remain disciplined. Balancing portfolios with a mix of growth sectors like technology and more defensive plays like energy and gold will be key to navigating the current environment. The road ahead may be uncertain, but with careful allocation, there are opportunities for outperformance in today’s market.